In 2026, the financial landscape continues to evolve, and unexpected expenses are a part of life. Whether it’s a job loss, medical emergency, or urgent home repair, having an emergency fund is more crucial than ever. An emergency fund is your financial safety net - it helps you manage unforeseen costs without relying on high-interest loans or credit cards.

Financial experts recommend that everyone start saving for emergencies to build a safety net that covers unexpected expenses.

Why an Emergency Fund Is Essential in 2026

Having an emergency fund provides several key benefits, offering you both financial stability and the ability to handle unexpected situations confidently. The best time to start saving for emergencies is today, even if you begin with small, consistent contributions.

Having an emergency fund provides several key benefits, offering you both financial stability and the ability to handle unexpected situations confidently. The best time to start saving for emergencies is today, even if you begin with small, consistent contributions.

1. Protection Against Unforeseen Events

Life is unpredictable. No matter how well you plan, unexpected expenses will arise. Whether it’s a sudden medical issue, an urgent car repair, or an unexpected job loss, these events can strain your finances. Without an emergency fund, you may have to borrow money or use credit cards, which can lead to debt accumulation and financial stress. An emergency fund helps you cover these expenses without derailing your financial health.

In 2026, with the global economy in flux, having a cushion against potential financial disruptions is even more important. Whether due to inflation, healthcare costs, or job insecurity, an emergency fund can serve as a safeguard for your personal finances.

2. Reduces Financial Stress

Financial stress can negatively impact your mental and physical well-being. Constantly worrying about unexpected expenses can create anxiety. Having an emergency fund gives you a sense of security, knowing that you have resources available to cover immediate expenses without scrambling for solutions. It’s one less thing to worry about in times of uncertainty.

3. Helps Avoid Debt

Emergencies often require immediate attention, and without savings to cover the costs, you may resort to borrowing money. This leads to credit card debt, high-interest loans, or even payday loans, all of which can significantly affect your financial future. By having an emergency fund in place, you avoid these situations and prevent falling into debt, which can take years to pay off.

Emergencies often require immediate attention, and without savings to cover the costs, you may resort to borrowing money. This leads to credit card debt, high-interest loans, or even payday loans, all of which can significantly affect your financial future. By having an emergency fund in place, you avoid these situations and prevent falling into debt, which can take years to pay off.

4. Provides Financial Flexibility

Having an emergency fund provides you with flexibility when unexpected opportunities arise. For example, you might have the chance to take on a new job or invest in a business opportunity but need to relocate or make a significant purchase. An emergency fund gives you the financial freedom to make these decisions without the added burden of financial pressure.

How Much Should You Have in Your Emergency Fund?

The amount you should save in your emergency fund varies based on your lifestyle, monthly expenses, and risk factors. Before you start saving for emergencies, calculate at least three to six months of essential expenses to set the right goal. However, a common rule of thumb is to save three to six months' worth of living expenses.

Three months’ worth: If you have a stable income and job security, three months of expenses may suffice.

Six months’ worth: If you have an irregular income, own a business, or work in an unstable industry, six months’ worth of expenses might be a safer goal.

Consider all your fixed expenses, including rent or mortgage payments, utilities, food, transportation, insurance premiums, and debt payments. By having a comprehensive view of your monthly spending, you can determine how much you should aim to save.

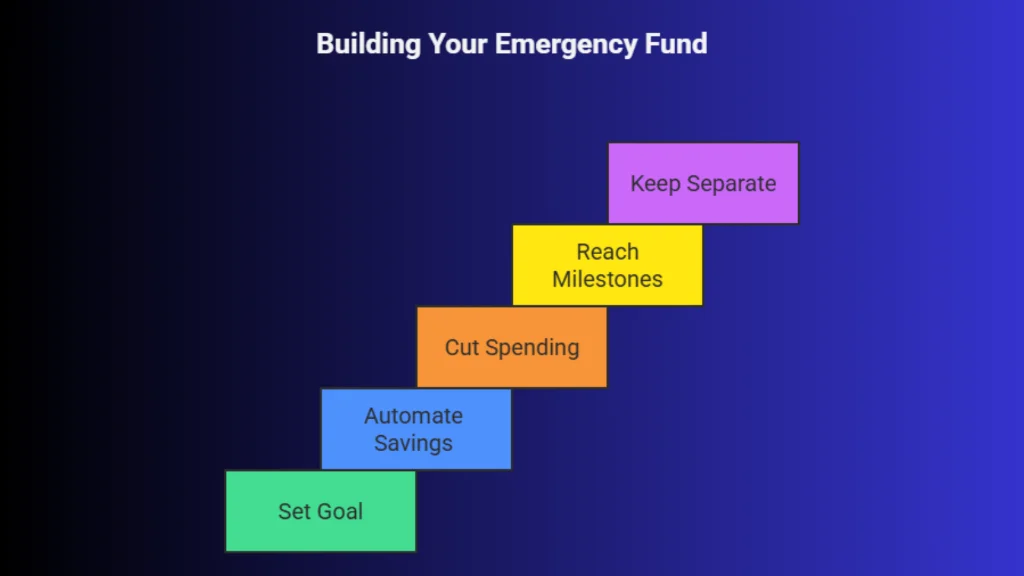

How to Build Your Emergency Fund

Building an emergency fund takes discipline, but it’s one of the most important steps you can take to secure your financial future. Here are a few steps to help you start:

Building an emergency fund takes discipline, but it’s one of the most important steps you can take to secure your financial future. Here are a few steps to help you start:

1. Set a Realistic Savings Goal

Begin by setting a clear savings target. Depending on your monthly expenses, determine how much you need to save to reach your goal. Break this down into monthly savings targets. For example, if you want to save $12,000 in 12 months, you’ll need to save $1,000 per month.

2. Automate Your Savings

The easiest way to build an emergency fund is by automating your savings. Set up automatic transfers from your checking account to a high-yield savings account specifically designated for emergencies. This way, you pay yourself first before spending on non-essential items.

3. Cut Back on Non-Essential Spending

If you’re struggling to reach your emergency fund goal, consider cutting back on discretionary expenses. This may include reducing dining out, canceling unused subscriptions, or finding cheaper alternatives for regular purchases. These small changes can add up quickly and help you build your fund faster.

4. Start with Smaller Milestones

Building an emergency fund can feel overwhelming, especially if you’re starting from scratch. Start with a small, attainable goal, such as $1,000, and gradually increase it as you get more comfortable with saving. Once you’ve reached that initial milestone, you’ll feel more motivated to continue saving.

5. Keep Your Fund Separate

To prevent the temptation to dip into your emergency fund for non-emergencies, keep it in a separate account. Consider using a high-yield savings account, where your fund can grow with interest over time. Avoid using this account for regular expenses.

Conclusion

An emergency fund is one of the most important financial tools you can have, providing stability, peace of mind, and protection from unforeseen financial challenges. In 2026, with the economy in constant flux, having a well-funded emergency reserve is more crucial than ever.

Start small, stay consistent, and build your fund over time. Whether you're just beginning or need to replenish your savings, having an emergency fund will give you the flexibility and security to navigate any unexpected events that come your way. Many users choose high-yield savings accounts when they start saving for emergencies, as they offer liquidity and better returns than regular savings accounts.

Preparing for emergencies doesn’t have to mean breaking your investments, learn how Loan Against Mutual Funds (LAMF) can help meet short-term needs while keeping long-term goals intact.