Creating a financial plan for the next five years is one of the most effective ways to ensure long-term financial success. A well-crafted 5-year financial plan helps you define your financial goals, track your progress, and stay on course to achieve your financial aspirations. Whether you’re looking to pay off debt, save for retirement, or make large purchases like a home, having a clear plan in place is crucial. To create a financial plan, you must carefully evaluate your current income, fixed and variable expenses, existing savings, outstanding liabilities, and future life goals such as education, home ownership, or retirement.

In this blog, we will guide you through the steps to create a comprehensive 5-year financial plan, offering practical tips and advice to help you manage your money, set goals, and secure your financial future.

Step 1: Set Clear Financial Goals

The first step in creating a 5-year financial plan is to establish clear, measurable financial goals. These goals will act as the foundation of your plan and provide direction as you move forward. Young professionals who create a financial plan early in their careers gain a strong advantage because they can start compounding their investments sooner while maintaining better control over spending habits. Start by categorizing your goals into short-term, medium-term, and long-term objectives.

Short-Term Goals (1-2 years)

Short-Term Goals (1-2 years)

Pay off high-interest debt (credit cards, loans)

Build or grow an emergency fund

Start saving for large purchases, such as a vacation or a car

Medium-Term Goals (3-5 years)

Save for a down payment on a home

Increase retirement savings

Invest in an education or professional development

Long-Term Goals (5+ years)

Save for retirement

Achieve financial independence

Build wealth through investments

By setting specific, measurable, achievable, relevant, and time-bound (SMART) goals, you create a solid foundation to track your progress and stay motivated.

Step 2: Assess Your Current Financial Situation

Before you can build a 5-year financial plan, it’s essential to understand where you currently stand financially. Take an inventory of your assets, liabilities, income, and expenses. This will help you assess your current financial health and identify areas where you need to make improvements.

Key Areas to Review:

Income: What are your sources of income (salary, business earnings, investments)?

Expenses: What are your fixed and variable expenses (housing, utilities, groceries, entertainment)?

Debt: How much debt do you have (credit cards, student loans, mortgages)?

Savings & Investments: What do you have in savings and investments (retirement accounts, emergency fund, investment accounts)?

By assessing your financial situation, you’ll get a clear understanding of where you are and how much progress you need to make toward your goals.

Step 3: Create a Budget and Manage Your Expenses

Once you’ve assessed your financial situation, the next step is to create a realistic budget that aligns with your financial goals. A well-structured budget allows you to allocate your income toward savings, debt repayment, and investments, while also managing your daily expenses. Before committing to major financial decisions like investing in equities, buying property, or taking large loans, it is essential to create a financial plan that balances growth, safety, and liquidity.

Once you’ve assessed your financial situation, the next step is to create a realistic budget that aligns with your financial goals. A well-structured budget allows you to allocate your income toward savings, debt repayment, and investments, while also managing your daily expenses. Before committing to major financial decisions like investing in equities, buying property, or taking large loans, it is essential to create a financial plan that balances growth, safety, and liquidity.

Key Budgeting Tips:

50/30/20 Rule: Allocate 50% of your income to essentials (housing, utilities), 30% to discretionary spending (entertainment, dining out), and 20% to savings and debt repayment.

Track Your Spending: Use budgeting apps or spreadsheets to track your monthly spending and identify areas where you can cut back.

Adjust for Goals: Make sure your budget includes contributions toward your savings and investment goals. If you want to save for a down payment or retirement, prioritize these goals in your budget.

A budget helps you stay disciplined and ensures you’re making the most of your income as you work toward achieving your 5-year financial goals.

Step 4: Create a Debt Repayment Plan

If you have debt, it’s important to create a clear plan for paying it off while building wealth. High-interest debt, such as credit card balances, should be paid off as quickly as possible to avoid accruing unnecessary interest charges. On the other hand, low-interest debt (like a mortgage or student loans) can be managed over a longer period.

Debt Repayment Strategies:

Debt Snowball Method: Pay off your smallest debts first, then move on to larger debts as you build momentum.

Debt Avalanche Method: Focus on paying off the debts with the highest interest rates first to minimize the total interest you’ll pay.

Having a plan for debt repayment ensures that you reduce liabilities over time, freeing up money for savings and investments.

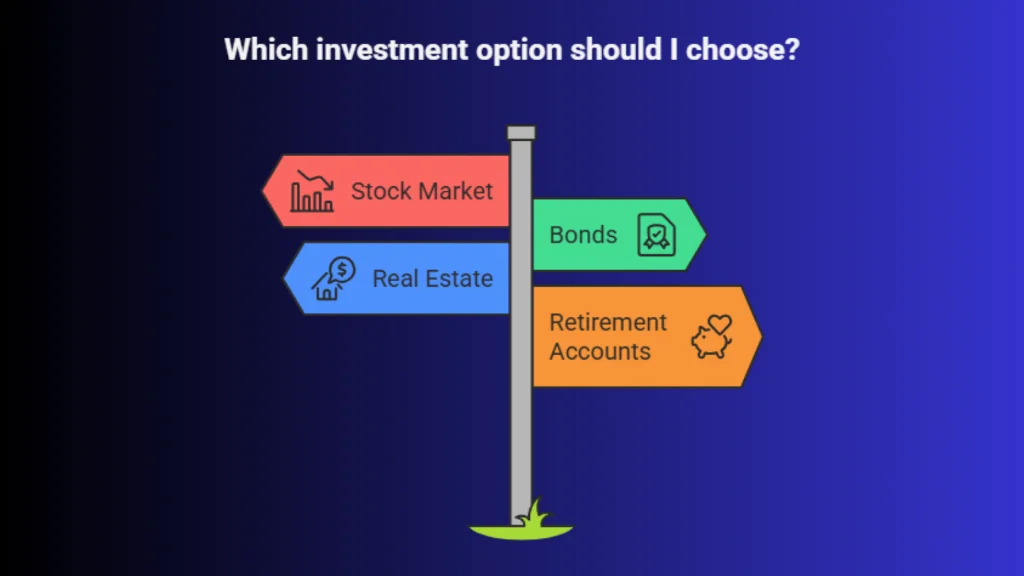

Step 5: Build an Investment Strategy

Investing is a key component of any financial plan, and it’s especially important when working toward long-term wealth-building goals. You can create a financial plan that actually works by clearly defining short-term and long-term goals, building an emergency fund, selecting suitable investment instruments, and reviewing progress regularly. In a 5-year financial plan, your investment strategy should be aligned with your risk tolerance and financial objectives.

Investment Options to Consider:

Stock Market: Investing in stocks, ETFs, and mutual funds offers the potential for higher returns but also comes with higher risk.

Stock Market: Investing in stocks, ETFs, and mutual funds offers the potential for higher returns but also comes with higher risk.Bonds: Bonds are generally considered safer than stocks and can provide steady income through interest payments.

Real Estate: If you plan to buy a home or invest in property, real estate can be a valuable asset class.

Retirement Accounts: Contribute to retirement accounts like a 401(k) or IRA to take advantage of tax benefits and build wealth for the future.

The key is to diversify your investments and create a strategy that aligns with your financial goals and timeline.

Bottom Thoughts

Creating a 5-year financial plan is an essential step toward achieving your financial goals and securing your future. By setting clear goals, assessing your current financial situation, budgeting wisely, paying down debt, and investing for long-term growth, you can build a solid foundation for your financial journey.

Families that create a financial plan with proper insurance coverage, tax planning, and diversified investments are better equipped to handle unexpected financial shocks and long-term wealth creation.

A well-structured financial plan keeps you on track and helps you stay focused on your goals, even when life presents financial challenges. Create a disciplined 5-year financial plan, with Loan Against Mutual Funds (LAMF) offering flexibility to manage cash needs without disrupting investments.